In the high-stakes world of commercial insurance, data is oxygen. But for too long, carriers have been choking on the very thing they need to survive. The problem isn't a lack of data—it’s the 'Integration Nightmare.'

As an industry veteran and technologist, I’ve seen it time and again: A carrier buys a cutting-edge risk scoring tool or subscribes to a new geospatial data feed. But then, the reality sets in. The data sits in a silo. To get it into the underwriting workflow requires a six-month IT project, custom API development, and ongoing maintenance. By the time the integration is live, the market has moved on.

To truly modernize, we need to stop treating integration as an engineering hurdle and start treating it as a seamless, invisible utility.

The New Standard: Integration Without the Headache

For an underwriting system to be truly 'intelligent,' it cannot be an island. It must be a hub. The next generation of underwriting isn't just about processing submissions; it's about instantly enriching them with credit reports, climate data, financial health checks, and freight analytics—without the underwriter leaving their screen.

This is where the concept of 'Agentic AI' and robust connectivity protocols (like MCP, A2A) come into play. But these advanced tools are useless if they can't 'speak' to the outside world effortlessly.

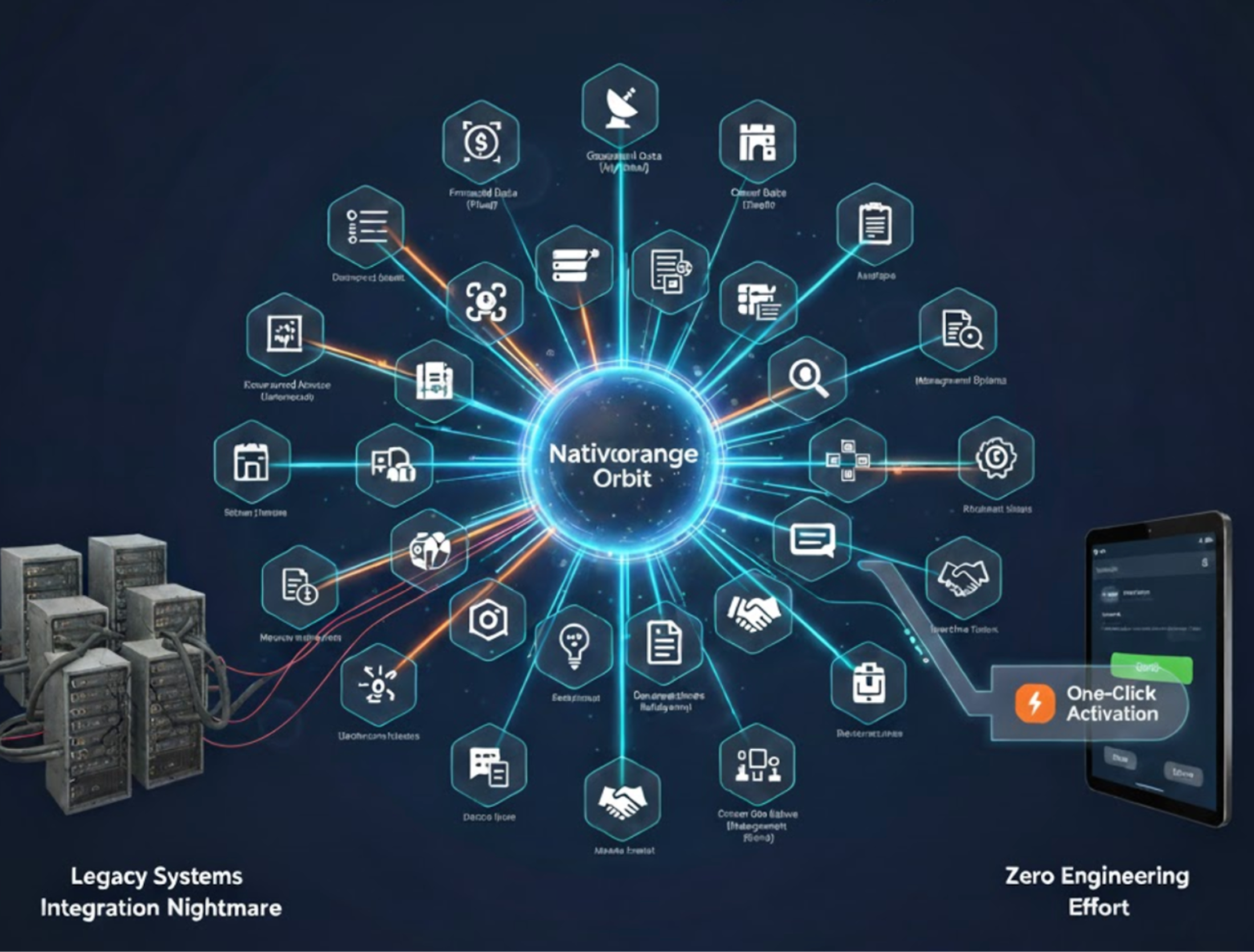

Enter Orbit: Nativeorange's One-Click Integration Engine

This is why I am incredibly excited about Orbit, the new partner integration platform from Nativeorange. Looking at its capabilities, it is clear that Orbit is designed to solve the 'IT Bottleneck' once and for all.Orbit isn't just an API marketplace; it is a dynamic connectivity layer that allows carriers to activate powerful 3rd-party integrations without lifting a finger.

Here is how Orbit changes the game for carriers:

1) The 'Zero Engineering Effort' Promise

Traditionally, adding a partner like Plaid for financial data or MyRadar for weather intelligence would require your engineering team to read documentation, build connectors, and test endpoints. Orbit flips this script. It offers a 'One-Click' activation. You select the data provider, input your API keys, and the integration is instantly live within your Nativeorange Underwriting Bench. No code. No IT tickets.

2) Powering the Agents

We talk a lot about 'Agentic AI'—autonomous agents that can assess risk and quote policies. But an agent is only as good as the data it can access. Orbit acts as the nervous system for these agents. By standardizing connections to over 40+ trusted data APIs (covering everything from Claims to Credit), Orbit ensures your AI Agents have real-time access to the ground truth they need to make complex decisions.

3) Future-Proofing with A2A, MCP and Open Protocols

Orbit is built to support the future of connectivity. Whether via traditional REST APIs or modern frameworks like Agent to Agent (A2A), Model Context Protocol (MCP), Orbit abstracts the complexity away from the carrier. It handles the translation, security, and data mapping in the background, delivering clean, enriched data directly into your decision-making workflow.

4) The Bottom Line for Carriers

The competitive advantage in insurance is no longer just about who has the best actuarial models; it's about who can deploy new data sources the fastest.

With Orbit, Nativeorange has removed the friction. You get instant access to a growing ecosystem of partners—like Ricoh for document intelligence and Carrier Software for seamless management system data flow—allowing you to reduce costs, eliminate technical debt, and focus on what matters: writing profitable business.

The future of underwriting is connected, and with Orbit, that connection is finally just a click away.

Please reach out or visit https://nativeorange.ai/orbit/